Through the Noise interviewed Elizabeth Scott, CEO of Brighter Strategies, to help nonprofit employers improve their overall effectiveness by building their internal capacity. Listen below or check out the full library of podcasts.

Podcast Description: This podcast emphasizes the importance of harnessing the emotional intelligence of staff members so that organization can do the most with what they have. Dr. Elizabeth Scott aims to provide thought leadership and high value organizational development consulting in an effort to strengthen the nonprofit sector.

Brighter Strategies is a non-profit consulting firm that works with non-profit organizations as a “thought partner” to help build capacity and make the most of their greatest asset—their human capital. To learn more about Brighter Strategies, visit their website at www.brighterstrategies.com.

To stay up-to-date on the latest best practice tips and cost-saving ideas just for nonprofits, sign up for UST’s monthly eNews: https://www.chooseust.org/enews

Total non-farm payrolls increased by 156,000 in September which was lower than the expected 176,000. So far this year, job growth has averaged 178,000 per month, compared with an average of 229,000 per month in 2015. The unemployment rate ricked slightly upwards to 5.0 percent and the number of unemployed, at 7.9 million, changed little. Both measures have shown little movement since August of last year.

Job gains occurred in professional and business services with 67,000 new positions while health care added 33,000 jobs and food and bar services added 30,000. Retail trade continued to trend up over the month with an addition of 22,000 jobs.

Mining employment was unchanged in September and employment in other major industries, including construction, manufacturing, wholesale trade, transportation and warehousing, information, financial activities, and government, showed little change over the month.

The number of long-term unemployed (those jobless for 27 weeks or more) accounted for 24.9 percent of the unemployed population and remained unchanged at 2.0 million. Both the labor force participation rate, at 62.9 percent, and the employment population ratio, at 59.8 percent, were unchanged in September.

Average hourly earnings for all private non-farm employees rose by 6 cents to $25.79. Over the year, average hourly earnings have risen by 2.6 percent.

The Federal Reserve is looking to get rates back to normal and there is implication that could happen in December so this report comes at a critical time. With the presidential election, however, there may be further postponement.

UST R ewards 431 Members for Successfully Lowering Their Anticipated Unemployment Claims within the Last Year.

Santa Barbara, CA (October 4, 2016) – In an era when nonprofits are struggling to stretch their budgets, the Unemployment Services Trust (UST) today announced it is pleased to disperse $6,664,166 to 431 of its program participants. The agencies receiving the funds have demonstrated prudent management of their unemployment costs resulting in a return of funds back to the organizations. This brings participant savings over the past year to a whopping $34,980,275.96 in claims savings, audited state returns and cash back.

501(c)(3) organizations have the exclusive advantage of opting out of their state’s unemployment tax system and instead paying dollar-for-dollar for only their former employees claims. Excess payments made into the state tax system are not refunded to employers. UST, however, provides cash back when an organization has had a positive claim history and has reduced its unemployment claims lower than initially anticipated, while also staying well-funded for future claims.

“It’s incredibly rewarding to be able to give money back to these organizations whose core mission objectives are geared towards serving their communities,” said Donna Groh, Executive Director of UST. “It allows them the funds to further expand their programs in areas where otherwise they might not have been able. In a way we’re helping to invest in the future of each nonprofit organization participating in the Trust and that’s a great feeling.”

The largest nonprofit unemployment trust in the nation, UST helps 501(c)(3) organizations nationwide save time and money through a host of workforce management solutions that include – unemployment claims management, cash flow protection, HR Workplace assistance, outplacement services and more. The company services nonprofits from all sectors with 10 or more full-time employees. UST encourages nonprofits that are currently tax-rated or direct reimbursing on their own to review their options as they may be over-paying.

From day one and onward, nonprofit employees look to training to feel capable at their job… and valued. Do you offer them that opportunity?

According to the 2015 Nonprofit Employee Engagement and Retention Report, organizations with high turnover also tended to have fewer training opportunities for employees—so providing new hires with the right tools at the right time is extremely important for retaining good-fit employees.

Employees want to feel like they’re making a contribution, and being trained on the job is a critical part of employee development and reinforcing their sense of worth. But in last year’s study, 29% of nonprofit respondents reported that they received NO onboard training, and about 1/3 said they got only 1-2 weeks.

Longer onboard training for new employees was linked to 1) lower turnover, 2) higher levels of employee job satisfaction, and 3) a lower likelihood of employees planning to quit in the next year. Organizations with 90-day onboarding strategies had the highest employee engagement. And when a company implements a successful onboarding program, they experience 54% greater productivity and 50% greater retention.

Here are 4 simple ways you can implement training at your nonprofit:

Overall, onboarding new employees (especially supervisors) can help them feel welcome and prepared to do their best. Ongoing training is a great way to develop skills, maintain goodwill among employees and keep your new hires from packing up their desks.

Discover a few other top reasons your employees might be headed for the door. For a limited time, download UST’s 2016 report, 6 Reasons Your Nonprofit Employees QUIT, and learn how you can improve your organization’s employee management strategies.

HR professionals across all industries have been expressing concern over the difficulty in recruiting qualified job candidates for some time but with a lower number of applicants actually applying, the task of locating individuals who possess the needed skills, experience and educational credentials, is becoming even more challenging in the current day.

The fact that organizations are saying they have had more difficulty filling full-time regular positions in the last 12 months than in previous years is a sign that conditions have changed. The top cited reasons – lack of sufficient work experience and job skills among job candidates, more competition from other employers and a lower number of applicants’ altogether.

A skills shortage occurs when there are not enough people with a particular skill to fill the needed number of positions within a particular occupation. Some basic skills shortages are writing, basic computer skills, reading comprehension and mathematics. And applied skills shortages are critical thinking and problem solving, work ethic, written communication and leadership. With that said, the most difficult positions to fill were for high-skilled medical (nurses, doctors, specialists), scientists and mathematicians, skilled trades (electricians, carpenters, machinists), engineering and architecture, IT/computer specialist (analysts, developers, programmers) and executives. Basic and applied skills are not only critical but necessary in order to build a foundation for a strong and stable workforce.

Many organizations have had to have their training budgets increased in order to fill the gap between qualified candidates and or training existing employees. While online training courses have become the most utilized option, many employers are still utilizing conferences and professional workshops and on the job training. Investing in education and training should be viewed as a way to meet skills shortfalls.

Though many organizations are utilizing social media and collaborating with educational institutions as recruiting strategies, the most effective strategies have been using a recruitment agency and training existing employees to take on hard-to-fill positions.

Organizations need not to only focus on finding and retaining highly skilled employees but also need to consider how they are going to develop the next generation of organizational leaders as the current workforce ages and the highly experienced and skilled workers retire. Making sure employees are not at risk of burnout will also be critical, taking into consideration that when they’re unable to fill some positions, their existing staff may be forced to do more with less.

Question: What are some tips for developing and conducting an employee engagement survey?

Answer: An employee engagement survey can be a great tool to check the temperature of your culture. When done right, the survey can help you understand the needs of your employees, which in turn benefits productivity, job satisfaction and supports employee retention. It is also an excellent tool to help you calibrate the quality of your leadership as well as your employee relations and talent management programs.

Before you start, however, ensure that the management team is ready to act on the critical feedback you’ll get. Then decide what it is you need to know. Do you want to better understand how your employees view their relationship with management, understand and support the company’s strategic direction, or learn what aspects of their work environment, compensation and benefits, work assignments, and opportunities for learning and advancement are working (or not working)?

Next, determine how you will create, disseminate, tabulate, and communicate the survey process and results. If you’re creating your own survey, consider gathering employees from different areas of the company to formulate the survey questions and include them in the employee communications process to encourage participation. This team can also be instrumental in reviewing the survey results and providing feedback about how those results should be communicated and acted upon.

Another option is to use one of the many online engagement survey tools available in the marketplace. While the questions may not be as personalized to your company issues, you can get the surveys, along with the tabulated results, done quickly.

If you do create the survey in-house, consider these best practice tips:

Encourage participation by using incentives or contests. With more feedback, you’ll have a better picture of your employees’ engagement level. Train your leaders so that they are prepared to use the survey feedback as a gift to improve performance and have productive feedback and performance improvement planning sessions.

Most importantly, don’t ask for employee feedback unless you are willing to do something with the results. Your employees will expect you to implement changes and take action. Let them know how much you value and respect them by listening and acting on their opinions and ideas.

Q&A provided by ThinkHR, powering the UST HR Workplace for nonprofit HR teams. Have HR questions? Sign your nonprofit up for a free 30-day trial here.

Through the Noise interviewed Nicolie Lettini and Cathy Galbraith, CEO/Founder and Managing Director of CostTree, to help nonprofit employers better understand the difference between direct and indirect costs and how to accurately anticipate and budget for them annually. Listen below or check out the full library of podcasts.

Podcast Description: This podcast explains the importance of understanding where your nonprofit’s hard-raised money is going, and how you might be able to better allocate funds to your staff’s paychecks. Cathy Gallbraith constantly aims to help nonprofits understand how to create an indirect cost rate, how to use it in everyday strategic development and how to ensure organizational accountability and sustainability.

A cloud-based cost allocation software that simplifies the process of creating an indirect cost, CostTree looks to maximize the efficiency and effectiveness of entities that make a difference in our lives and the communities they serve. To learn more, visit CostTree’s website at https://www.costtree.net.

To stay up-to-date on the latest cost-saving ideas and best practice tips just for nonprofits, sign up for UST’s monthly eNews: https://www.chooseust.org/enews

August has continuously undershot expectations by the most of any month on average over the last 13 years and this year has proved no different with a mere 151,000 job gains. The unemployment rate was unchanged for the third month in a row at 4.9 percent and the number of unemployed persons held steady at 7.8 million or 9.7 percent – both showing little movement over the year. Average hourly earnings in August rose by an additional 3 cents to $25.73.

Employment in restaurants and bars continued to trend upward with an additional 34,000 jobs. Social assistance added 22,000 positions, with most of the growth in individual and family services. Employment in professional and technical services grew by 20,000 and financial activities edged up by 15,000. Health care also contributed 14,000 jobs in August, though at a slower pace than the average monthly gain over the prior 12 months. Since peaking in September 2014, employment in mining has declined by 223,000, with an additional loss of 4,000 positions in August.

Employment in several other industries – including constructions, manufacturing, wholes trade, retail and information, transportation and warehousing, temporary help services, and government – showed little change over the month.

The number of long-term unemployed (those jobless for 27 weeks or more) accounted for 26.1 percent of the unemployed population and remained unchanged at 2.0 million. Both the labor force participation rate, at 62.8 percent, and the employment-population ratio, at 59.7 percent, were also unchanged in August.

The change in total nonfarm payroll employment for June was revised down from +292,000 to +271,000, and the numbers for July were revised up from +255,000 to +275,000, combined job gains were 1,000 less than previously reported.

Job numbers are being watched closely by the Federal Reserve as they prepare to meet this month to discuss the possibility of a rate increase which is appropriate when the economy shows a solid and continual improvement. Many feel the August numbers still show economic growth but the jobs report likely decreases the probability of a rate hike for right now.

Although we always suggest starting your search for free or reduced cost supplies and services by talking to state and national associations (check out our 80+ association partners here), sometimes you need more.

Looking for extra technology resources?

Check out Techsoup, Google for Nonprofits, Microsoft’s Technology for Good program, the Salesforce Foundation, and Citrix, all of which provide free or discounted tech services to nonprofits.

Looking for financial management help?

Check out The Wallace Foundation, which offers helpful resources on planning, monitoring, operations, and governance.

Also check out 501Commons, which has assembled a vast library of tools & best practices for nonprofits, and the Nonprofits Assistance Fund which was specifically created with the goal of helping other nonprofits thrive.

Want to help your employees achieve their professional dev elopment goals?

The Stanford Social Innovation Review makes select webinars for professional development available for free. And, since the Review is constantly adding new things, they offer a great way to continuously access up-to-date information and resources.

Need nonperishables like apparel, books, toys, personal care products, or office and school supplies?

Good360 has been helping connect companies with nonprofits that need inventory that the retailer has found to be slow-moving, obsolete, and seasonal since 1983. Now, Good360 is considered the nonprofit leader in product philanthropy and distributes goods on behalf of America’s top brands.

Still need more?

Other sites like Grassroots.org, which provides information about free resources to help charities, provide a wide array of resources in one place from team collaboration tools to project tools to marketing and administrative tools. Similarly, the Foundation Center provides a resource called the “Nonprofit Startup Map” which localizes links to state resources on a state-by-state U.S. map.

Want more free resources? Run a quick Google Search for the term “free resources for nonprofits” and see what you come up with!

These mistakes can be costly if you’re not careful; think compliance penalties, litigation, unemployment costs and employee replacement costs. We’ve listed some of the most common mistakes so you can try to avoid them at your nonprofit.

1. Bad Hiring Decisions

In the nonprofit world, you’re likely to know just about everyone who works in the same circle. So it makes sense that to offer a job to someone you know, right? Well sometimes skipping the interviewing step means you’re missing out on the most qualified candidate, and missing important information. Interviews, background checks and references are absolutely a must when it comes to hiring the right person. The wrong person for a position can be costly, since you may have to pay unemployment if you have to replace them, and the cost in both time and money to find a replacement quickly adds up.

2. Not Documenting Infractions

It’s not easy addressing performance or company policy concerns with an employee. Although it can be uncomfortable, it’s much more uncomfortable to have to address these issues in an unemployment claim appeal hearing when you try to prove the employee was discharged for cause. The first steps are having clear performance expectations in your job descriptions as well as an employee handbook outlining organizational policies. Then create a performance review to discuss any concerns with an employee, and address the steps they can take to improve. And any infractions must be documented in writing, including:

Finally, don’t wait to have the conversation! It’s easiest to provide immediate feedback and point to a distinct occurrence rather than try to explain later on “Remember that one time…” Do it now, and you’ll thank yourself later.

3. Not Knowing Basic HR Rules

If you don’t have someone with acute knowledge of the laws around the following HR laws, make sure you get acquainted with the rules or have a certified HR professional to help you:

Ignoring these laws can lead to costly legal concerns and thousands of dollars wasted. Download the 36 Critical HR Processes, and learn more about UST’s live hotline with SPHR and PHR certified HR professionals.

4. Not Knowing the Difference Between Contracted, Volunteer, Part-Time, and Full-Time Employees

The U.S. DOL has strict rules around Independent Contractors and Volunteers. Not only do you need to be aware of the rules around pay and benefits, you should know who is eligible to collect unemployment benefits. Independent contractors may file for unemployment, and you need to be able to prove he or she is not an employee of your company.

Here at UST we know it’s not easy managing the most important part of your organization: your human capital. Having the right employees can make or break your mission, and so can following the proper HR procedures. Interested in learning more about our tools for nonprofits? Find out about Unemployment Claims Administration and our HR Hotline.

Setting measurable goals and creating systematic procedures for leadership development programs will enable you to address leadership skill gaps at a more efficient pace. Follow these 4 steps to implement an effective leadership development plan, while gaining support from your current management team:

Discover more methods on how to create future leaders here.

But finding and hiring highly engaged employees is difficult. You might ask – How can an employee be “engaged” before they’re even hired? Well, the highly engaged employee is often a person who simply leans in that direction in all parts of their life. That’s why finding them is so important for your nonprofit – because it’s easier to help an engaged employee thrive than to try to build one from the ground up.

Here are some signs of a motivated personality when you’re looking at hiring, or even internal development:

1. They don’t expect their organization or their leaders to provide all the stimulation in their workday or their job. They seek out new opportunities to engage in their job on their own. Complaining about a former manager or job not providing enough work satisfaction in an interview can be a red flag that they didn’t take that extra step to engage themselves at their previous job.

2. They know their performance speaks for itself, and they’re not worried about what their organization can give them, but rather about what they can give to their organization. They have a low sense of entitlement. (Although rewarding and recognizing them is important to keeping them engaged!)

3. They help inspire others to love your mission, including clients and volunteers. They can’t help but be excited about what they’re doing and that translates to others.

4. They are engaged despite the conditions around them. Even if their last job wasn’t perfect, they found ways to be engaged. And even motivation in other places of their life can show an “engaged” personality – like running a 5k to help a local dog shelter. Your job is simply to foster this engagement at work.

5. They enjoy shaping their own outcomes – and the outcomes of your organization. Being a voice in the direction of your organization, whether it’s something small like finding a better way to file invoices, or more strategic like new ideas for an annual campaign, they will feel happiest when they can give something to your organization.

6. They like to stretch the limits. This can be uncomfortable for leaders, but allowing engaged employees to think outside of the box can lead to some amazing results. And sometimes listening and showing you are truly interested in their input, even if it doesn’t get used in the end, shows that this behavior is not only welcome, it’s appreciated – and it should be!

A: The employer should contact the Employee Assistance Program (EAP) directly and request a review of the process for making referrals. In general, during the implementation process, the EAP provides the contracting employer with that information so that employees and employers have a clear understanding of the services the EAP can offer employees and the process by which the employer can make referrals to the service. This service typically includes employer assistance so that employers may communicate directly with the EAP counselor to provide a “heads up” to the counselor regarding the performance issue and obtain guidance for handling the discussion with the employee. Then the employer can have the performance discussion and refer the employee to the EAP as part of the action plan for performance improvement. Discussions between the employee and the EAP are confidential, and the employer should not expect feedback from the EAP regarding those discussions.

While the employer can make the referral, it is ultimately an employee’s choice whether or not to contact and work with the EAP. If the employee chooses not to seek help or address the issue that led to the referral in the first place and performance does not improve, then the employer should follow its progressive disciplinary process, including corrective action up to and including termination of employment.

Question and Answer provided by ThinkHR. Learn more about how your nonprofit can gain access to their expert HR staff here.

Sometimes it’s sudden, like an accident or health crisis, and other times it’s simply a short term window to prepare for a leader leaving—but it is always important to have a backup plan when it comes to a leader’s absence.

It’s called emergency succession planning, and it’s critical to your organization’s survival.

Like any good emergency plan (think of those fire drills as a kid in school) – there should be clearly laid out steps to your emergency succession plan. Ready to stop, drop, and roll? Here are some basic elements to any good leader succession plan:

Learn more about emergency succession planning in this report.

Here are a few ways you can maintain an ethical culture at work:

Because nonprofits are often small organizations working in a small sector, their reputations are precious. Creating and implementing a strong ethical culture where employees maintain integrity will improve internal morale and help the overall business grow.

Learn more about how to encourage strong ethics within a work environment here.

Here at UST, we believe hiring the right employees is one of the top ways to reduce your organization’s overall unemployment costs. That’s why we’re committed to this blog, and giving nonprofits the tools they need to reduce turnover, reduce costs, and reduce time spent managing them! We also want to make sure nonprofits aren’t overpaying for unemployment taxes. You can find out by filling out a (free) savings evaluation here.

Even your strongest staff members can be negatively influenced when working with bad employees. Pairing others with someone who is unmotivated and performing inadequately can cause a domino effect of poor performance—making the overall business suffer.

Poor employees could chase away top performers

Top tier employees want to work with others who are just as driven and focused as they are. When talented workers see poor behavior or lack of contribution go unnoticed, they will begin looking for alternative job opportunities—ones where they can work with other high performers and feel more appreciated.

Low performers take up valuable space

By keeping low performing employees, you could be missing out on a new crop of talent. But how can you hire these rockstar candidates if there are no available roles at your organization? Making room for strong individuals who are willing to take initiative and contribute to the team is imperative when building a strong organizational foundation.

Because nonprofits often work with limited budgets and resources, developing and retaining a top-notch staff is key to successfully attaining mission objectives. And while it’s never an easy task to fire a bad employee, you’re doing what’s necessary as a leader to keep your organization moving forward.

Learn more about talent development strategies here.

A: Unless there is an employment contract or collective-bargaining agreement that suggests otherwise, employers do have the ability to set an employee’s work hours and job duties based on business needs. In the situation you described, you have a poor performer whom you want to transfer to another position, enhance the job, and bring in another employee to do the work. We assume that you have been addressing the current incumbent’s poor performance issues and the job that you are moving the employee into will be more in line with his or her skills and hopefully provide an opportunity for the employee to be more successful on the job. If you have not addressed your performance concerns, now is the time to do so. Explain why the change is necessary and use the opportunity to discuss the employee’s career goals and development needs. It is critical that the employee receive feedback regarding performance and behavior, as this may continue into either role and should be addressed to correct the concerns or take progressive discipline as appropriate. Have these conversations before you announce the new employee transferring into the expanded position.

The employee may have questions regarding why you are taking a part-time position and turning it into a full-time one and may suggest that he or she could be successful in the job if allowed the additional time each day to complete the duties. Be prepared to address that and provide the employee with a copy of the expanded job duties and explain why he or she is not the right fit for that job. Having a direct and respectful conversation, with specific feedback and action plans to move forward, can go a long way to making the change successful.

Question and Answer provided by ThinkHR. Learn more about how your nonprofit can gain access to their expert HR staff here.

Follow these 6 simple methods to ensure a successful employee transition:

Taking the time to efficiently train your new employees on your nonprofit’s culture, strategic goals, and personal role expectations will not only help new hires adjust, but also strengthen your organization as a whole.

Learn more tips about how to manage new employees here.

A: Yes. You may wish to inquire as to what types of compensation information they need so that you are providing the detail and data that is relevant for their review and discussion. You will want to ensure the privacy of your employees’ personal information, such as concealing Social Security numbers, garnishments, etc.

Executives typically need relevant summary compensation information for decision-making with revenue and cost considerations. Reviewing the actual intent of how the data will be used may enable you to provide a summary report without revealing data that could potentially be perceived as inappropriate to reveal.

Question and Answer provided by ThinkHR. Learn more about how your nonprofit can gain access to their expert HR staff here.

This is the longest it’s taken in more than a decade, 13 years to be exact, says the Vacancy Duration Measure. Compared to the height of the Great Recession, that’s actually almost 10 days longer than it took to fill a job then, when it was at 15.3 working days, reports TLNT.

Why the lag in recruiting and hiring for organizations across the U.S.?

Recruiters say that candidates are driving the employment market as opposed to the organizations– being more picky about the positions they will accept and the compensation and benefits they are willing to take. When turning down an offer, top candidates say the reason is another offer. And employers that are slow to make an offer are losing out and having to start all over with their search.

Increasing turnover a factor

Turnover, as we’ve all seen in the nonprofit world, is also an ever-growing trend. While unemployment subsides, many qualified employees are more comfortable jumping from job to job (or from the nonprofit sector to the private sector). Voluntary separations are on the rise according to the DOL, which reported 2.7 million people quit their jobs in June.

And a larger number of vacant positions is putting a strain on organizations, which are in a more pressured state of recruitment than in years past. Now, when hiring, filling the position isn’t enough. To avoid more future turnover, organizations are having to look at employee engagement and job satisfaction with a closer eye. Succession planning is also critical to ensuring the organization can stay afloat when key employees leave or retire.

Employee training may be key

While candidates may feel more confident in their hireability and be more choosey, it’s also true that employers are being more selective as well—sometimes too much. The gap between an unqualified and a qualified candidate can sometimes be filled through on-the-job training. Looking for the right personal traits and attributes in a potential employee is more important than specific job knowledge for many positions. And finding the right person for the job, not just the right resume, can mean long-lasting job satisfaction and less turnover.

Answer: More than likely the frequent use of a restroom may be a serious health condition; however, one would look to the Americans with Disabilities Act (ADA) prior to counting this time against the Family and Medical Leave Act (FMLA) entitlement.

In general, when counting bathroom time against an employee’s FMLA entitlement, only do so if the frequency and duration extends beyond the employee’s normal lunch and break periods.

Question and Answer provided by ThinkHR. Learn more about how your nonprofit can gain access to their expert HR staff here.

A: This answer is based upon the fact that there is no specific employment contract in place that outlines specific reasons for termination of employment and that the employer has an employment-at-will policy in place that provides for termination at will based upon the employer’s discretion.

From the detailed description of the situation, this employer does have an internal disciplinary procedure in place that specifies termination of employment for performance. This error was made years ago and could have been detected if the employee had been conducting annual audits of the file, which was not done, compounding the error.

Although employers can terminate employment “at will”, there should always be a legitimate business reason for the termination that is well documented, nondiscriminatory and carefully considered in order to reduce the employer risk of liability from wrongful termination suits.

The employer should consider the following prior to making the final decision:

If the employer believes that the situation warrants termination of employment because it is well-documented, the employee has been properly trained, the supervision was adequate, and that this is a unique situation, then a termination is allowed, but we recommend confirming the decision with legal counsel prior to the termination.

Question and Answer provided by ThinkHR. Learn more about how your nonprofit can gain access to their expert HR staff here.

But slow down just a minute. Are you sure your organization is ready to hire more employees?

Although only your organization can determine if you’re actually ready to hire new employees, Inc. recommends answering the following questions about your organization, where you want it to go, and what is happening now.

What kind of organizational structure do you want?

Do you want your organization to grow extensively? Are you pretty happy with the size it is now, but unable to meet the demands of your mission with your current staff, or are you hoping to grow organically whenever the need arises?

Will you be able to slow down growth if you need to?

Not all organizations have significant control over how much growth they will experience in any given time. For instance, if your organization helps provide disaster relief to a specific area and the area suddenly experiences a large-scale disaster, your response must be immediate and decisive. Or, if your organization helps animals and takes part in a multi-county animal seizure, you must be able to provide shelter and care for all of the animals involved for the foreseeable future.

But if your organization works to help a select group of impoverished students succeed, it’s reasonable to expect that there will not be an unmanageable influx of students to your program in any given year.

Do you really need help?

Do any of your employees have extra time throughout their week or month that can be used to address some of the needs that you’d like to hire new employees for? If so, can these employees be trained to perform some of the needed tasks?

While it might not fully address your needs, it would cut down on organizational waste and potentially allow for a part-time position to be created in lieu of the more expensive full-time position.

Are you fully prepared to recruit, hire, and train more employees?

Our ThinkHR resources and your UST Customer Service Representative can help you ensure your organization is best positioned to do all three without exposing you to excess liability in the future.

Not yet a member? Learn more about the UST program here.

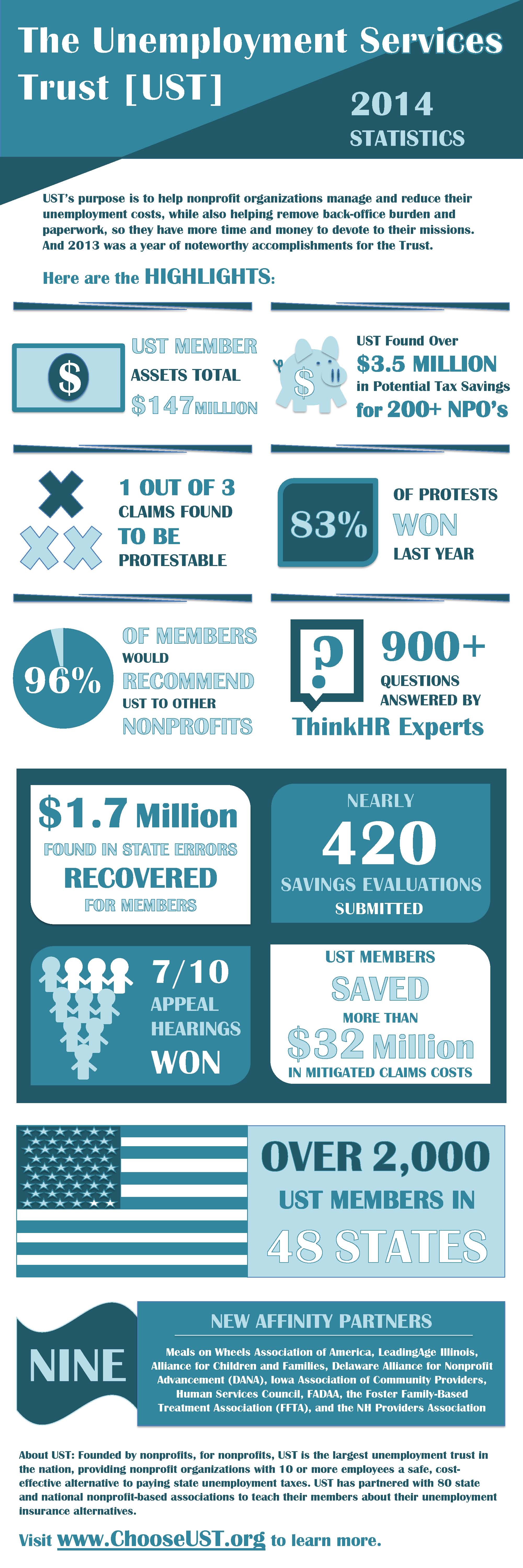

By offering access to an expert HR hotline, over 200 employee training courses, and a dedicated claims representative, UST helped its members uphold HR best practices, while remaining compliant with state laws. Last year, UST members saved more than $32 million in mitigated claims costs and won over 80% of their claims protests.

With a 96% recommendation rate, UST’s membership base and overall impact within the nonprofit sector continues to grow. Check out the full infographic for the full list of last year’s noteworthy accomplishments:

For a limited time, you can download the whitepaper for free and find out:

Learn the secrets of other nonprofit executives and HR staff who have reduced their human resource and unemployment claims costs. Download your complimentary copy of 5 Myths That Are Increasing Your Nonprofit’s HR Costs today.

By providing exclusive access to such cost saving resources, UST aims to educate 501(c)(3) organizations on the latest HR best practices and compliance laws—living up to its mission of “Saving money for nonprofits in order to advance their missions.”

Fill out a complimentary Savings Evaluation to find out if you can save with UST.

1. Get discounts by joining a nonprofit association. You can find one here. Most associations offer their members special benefits and discounts on everything from office supplies to insurance. In fact, UST is partnered with 80 national and state nonprofit associations whose members receive a waived enrollment fee when they join UST.

2. Get group discounts and share resources. If you can combine orders with other nonprofits or companies you work with or who share your building, you’ll receive better bulk pricing on all kinds of products. You can also share the costs of maintenance with others in the same building. You may even consider piggybacking on local businesses by asking if you can include your fundraising materials in their mailings. They may welcome the good will it generates for their company.

3. Is your organization a 501(c)(3)? Are there 10 or more full-time employees? If you answered yes to both, be sure to check out UST’s alternative to paying into the state unemployment tax system. It can save thousands annually because you no longer share in the state’s pooled tax system that is often driven by for-profit companies’ unemployment claims. Watch the one-minute informational video.

4. Save on printing. Today most people are used to receiving electronic communications in lieu of bulky printed pieces in the mail. Direct mail may still be an important part of your fundraising, but perhaps you can move to an e-newsletter to cut down on printing or provide electronic versions of your board book for board meetings. You can also use lower-weight paper to reduce printing and postage costs.

5. Try teleconferencing more often. Sometimes a video or phone conference is all you need to nail down specifics of a discussion, and it will save you big time on travel costs. (It works for job candidates and board members too!)

6. Save on employee training. Use videos, online training and/or another employee to provide training to new and existing employees. Self-paced training is typically best received by employees. And if you’re already a member of UST, you receive hundreds of online training courses for free through ThinkHR, which saves you about $6,000 annually.

7. Use public relations and social media to get free publicity. Talk to local media about covering an upcoming event, or provide guest columns or blogs to be published. And yes, you must be in the Twitter-verse nowadays for free PR. Don’t have an expert on staff? Recent college grads are a good place to look for social media expertise. Just make sure for interns or new hires that you create a social media policy so they don’t accidentally tarnish your reputation.

8. Use your board. Your board members should be part of your fundraising strategy. They should be able to help find sponsors for your events, and they shouldn’t be afraid to make the “ask” during fundraising season. In addition, they should be helping you find service providers and individuals who can provide the goods and services you need.

Got more ideas? Tell us on Facebook!