For nonprofit organizations, every dollar and every hour count. Balancing mission-driven work with administrative responsibilities can often stretch already limited resources. That’s where UST steps in.

For more than 40 years, UST has been dedicated to supporting nonprofits with workforce solutions designed to ease operational burdens, ensure compliance, and protect valuable funding. By offering cost-effective services tailored to the unique needs of nonprofits, UST empowers organizations to focus on what matters most: making an impact.

Today, UST proudly supports more than 2,200 nonprofit organizations across the country. These organizations span a wide range of missions, from social services and education to healthcare and community development, yet they all share a common goal—maximizing their resources to better serve their communities.

UST helps nonprofits achieve this by identifying opportunities to reduce unnecessary costs and improve operational efficiency. In fact, in just one year alone, UST refunded over $29 million to nearly 800 participating members—savings better served supporting critical programs, staffing, and services that directly support mission-driven initiatives.

One of the most challenging areas for nonprofits to navigate is unemployment claims management. Regulations can be complex, time-consuming, and costly if not handled properly. Without the right expertise, organizations risk overpaying or missing opportunities to dispute invalid claims. UST addresses this challenge with a comprehensive approach to unemployment cost management. By helping nonprofits better understand and manage unemployment-related responsibilities, UST ensures they only pay what they are legally obligated to—nothing more.

Strengthening Impact Through Strategic Partnership

A key component of UST’s approach is its strategic partnership with Equifax. Together, we provide nonprofits with expert unemployment claims management and hearing support, offering a powerful combination of experience, data insights, and proven processes.

This partnership enables nonprofits to:

In a new video featuring Equifax, viewers can learn more about how UST and Equifax work together to help nonprofits simplify unemployment claims management, reduce administrative burden, and identify opportunities for cost savings.

A Commitment to the Nonprofit Community

At its core, UST is more than a service provider—it’s a partner in helping nonprofits thrive. By combining decades of experience with innovative solutions and trusted partnerships, UST continues to deliver value where it matters most. As nonprofits face growing demands and evolving challenges, having the right support system in place can make all the difference. With UST and Equifax, organizations gain not only financial and administrative relief, but also the confidence that their resources are being used as effectively as possible.

Watch the video to learn more about how UST and Equifax are helping nonprofits reduce unemployment-related risk and protect resources that fuel their missions.

The Unemployment Services Trust (UST) is pleased to announce its new affinity partnership with the District of Columbia Behavioral Health Association. The D.C. Behavioral Health Association has chosen to pair up with UST to help their member organizations reduce unemployment costs and direct more funds toward mission advancement objectives.

This new partnership will allow 501(c)(3) organizations with 10 or more employees in the D.C. community to better take advantage of the federal law that allows nonprofits to opt out of the state unemployment tax system. By paying only the dollar-for-dollar cost of unemployment benefits paid to former employees, nonprofit employers that join UST lower their average claims cost to just $2,287 per claim versus the national average of $5,174 per claim.

“Nonprofits are often faced with smaller budgets and limited resources,” said Donna Groh, Executive Director of UST. “But last year, UST helped members achieve over $32.5 million in unemployment claims savings. We are thrilled to have the D.C. Behavioral Health Association join us as our latest Affinity Partner and look forward to helping their members maintain HR best practices and lower their unemployment costs.”

About D.C. Behavioral Health Association: D.C. Behavioral Health Association aims to expand and improve community-based behavioral health services through policy advocacy and staff development. All 42 members offer extensive services to the D.C. housing supports for adults and children in foster care, including treatments for substance abuse and mental health. For more information, visit www.dcbehavioralhealth.org.

About UST: The Unemployment Services Trust is dedicated to educating 501(c)(3)s about controlling HR and unemployment costs and helping them exercise their federal right to reimburse for unemployment claims, dollar-for-dollar. UST helps nonprofits manage unemployment claims to successfully save thousands of dollars annually. Learn more at www.ChooseUST.org.

Unfortunately, for many states, the realization came a little too late.

During the height of the Recession, almost 40 states borrowed a combined $50 billion from the Federal Unemployment Trust Administration (FUTA) to continue providing jobless benefits. This much debt required many states to make long-term changes to their unemployment systems by either charging penalties or fees to businesses or by cutting jobless benefits. Many made historic cuts to the number of weeks of aid available, but some—like New Jersey which racked up more than $1.5 billion in debt—took a long, hard look at the administration of their trust.

In New Jersey that long, hard look at the administration of their unemployment trust fund resulted in some spectacular results. Over the past four years New Jersey has identified more than 300,000 people who tried to wrongly collect benefits through identity theft, failure to report a new job, schemes, and honest mistakes. Also:

But what did New Jersey do that set them on the path to successfully rebuild their unemployment trust fund?

They updated their system.

Namely, they began using a strategy referred to as ‘identity proofing.’ With the help of LexisNexis, the state of New Jersey requires applicants to verify a wide range of personal information through a quiz on the state labor department’s website. The questions are specifically developed to be ones that the individual who owns an identity could accurately answer.

Then, using the billions of public records that LexisNexis collects, the answers—which range from what kind of car an applicant has, to who lives at their address—help weed out potential frauds.

Less than a year-and-a-half into the effort, more than $4.4 million in improper payments have already been stopped, and almost 650 instances of identity theft have been avoided.

Want to know how well your state is catching improper payments? The U.S. Department of Labor provides this state-by-state breakdown for 2013.

Read more about how New Jersey is fighting improper payments and unemployment fraud here.

The Department of Labor (DOL) provides a short overview of the program on their website, and summarizes it by saying: “Unemployment Insurance is a federal-state program jointly financed through Federal and state employer payroll taxes. Generally, employers must pay both state and Federal unemployment taxes…However, some state laws differ from the Federal law and employers should contact their state workforce organizations to learn the exact requirements.”

The program itself works to provide jobless workers who have lost their job through no fault of their own with temporary, partial wages while they search for a new position. For more information on how unemployment insurance works, read our more complete overview on the state program.

Is Your Nonprofit Liable?

501(c)(3) nonprofits are exempt from federal unemployment taxes, but may be liable for state contributions if they meet something called the “4 for 20″ provision. This provision is triggered when four or more individuals are employed on the same day for 20 weeks in a calendar year, though not necessarily for consecutive weeks. It is important to note that who is considered “employed” for these purposes is not always straightforward – see Independent Contractors below.

Why Independent Contractors May Still Be Considered Employees

There are different rules and tests used by government organizations to determine independent contractor status, because different organizations are responsible for separate aspects of law. For the purposes of unemployment insurance, the Department of Labor uses something called the “ABC test”, which makes it sound simple, but is more complicated when applied to real situations.

The ABC Test establishes criteria that an work relationship must meet in order to for the services of that individual to not be considered employment. The three parts of the ABC Test relate to employer control/direction of the worker, place(s) of business or courses of business, and proof that the worker is independently established in the trade. A nonprofit may have to pay unemployment taxes even if the IRS or their state revenue services determine that, for income tax purposes, individuals may be independent contractors.

Cost-Saving Alternatives

The Unemployment Services Trust (UST) provides an alternative to paying into the state unemployment tax system, and can be a cost-saving option for nonprofits with more than 10 employees. Through UST, organizations directly reimburse the state only for the claims of their former employees, rather than paying the state unemployment insurance tax which covers all employers throughout the states.

And, because keeping unemployment costs low is vital to so many organizations across the U.S., we’ve added state-by-state information for taxable wage bases from the Department of Labor so you can see where your organization falls on the tax scale.

We encourage nonprofits to be proactive in learning what their options are, and what types of unemployment tax alternatives best suit their needs. Complete a complimentary Savings Evaluation to see if your organization could save money on its unemployment costs.

This post does not constitute official or legal advice. A version of this article originally appeared on blog.nonprofitmaine.org by Molly O’Connell.

Over the next several weeks 521 nonprofit members of the Unemployment Services Trust (UST) will receive a combined $8,762,873 in cash back. In total this brings participant savings over the past year to more than $43 million in claims savings, audited state returns, and cash back.

“One of the most exciting times of the year at UST is when we get to tell members that they will be receiving money back,” said Donna Groh, Executive Director of UST. “For members that elect to take the cash back as a check this money often helps them expand important initiatives. And, learning the exact impact that each dollar we’re able to save, and return, to nonprofit employers helps motivate us to find even more ways to lower unemployment costs across the board for our members.”

The UST program, which helps nonprofits with 10 or more employees control unemployment-related HR costs, includes an annual review of its 2,000+ nonprofit accounts–using an advanced actuarial model. Unlike the state unemployment tax system or some private insurance where taxes and premiums cannot be refunded (even when benefits paid out are far below what the employer paid in), UST instead allows for cash back when an organization has a positive unemployment claim experience.

UST members whose claims were lower than anticipated, and that are well-funded for future claims, will receive a direct refund or credit to their nonprofit organization.

“Hearing the individual stories about what members plan to do with their cash back is extremely rewarding, and allows us to better emphasize the mission-driven impact of becoming part of the UST program,” seconded Adam Thorn, Director of Operations.

By aiming to ensure that a nonprofit is properly reserved for unemployment claims costs, but not holding excess funds beyond the necessary cushion for future claims, UST helps serve its mission of “Saving money for nonprofits in order to advance their missions.”

To learn more about the UST program for 501(c)(3) employers, visit www.ChooseUST.org or call (888) 249-4788 to speak with an Unemployment Cost Advisor.

About UST: Founded by nonprofits, for nonprofits, UST is the largest unemployment trust in the nation, providing nonprofit organizations with 10 or more employees a safe, cost-effective alternative to paying state unemployment taxes. UST has partnered with 80 state and national nonprofit-based associations to teach their members about their unemployment insurance alternatives. Visit www.ChooseUST.org to learn more.

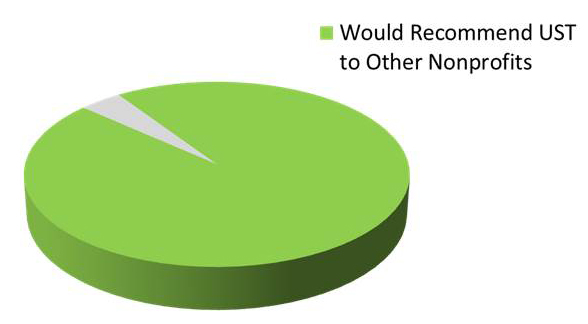

The Unemployment Services Trust (UST) is proud to announce that 96 percent of current participants would recommend the program as a valuable cost-saving opportunity for nonprofits. UST credits the improvement over last year’s 93 percent recommendation rate to an intense focus on the overall member experience and greater attentiveness to members’ needs.

“From the very beginning, the UST program was designed to support nonprofits by reducing the time and cost associated with managing an unemployment claim,” said Donna Groh, Executive Director. “To have found that our members would overwhelmingly recommend our service to other nonprofits is extremely rewarding.”

“We’ve worked hard to improve our customer service model and increase the quality of interactions that our customer service team has with our current members over the past year,” said Adam Thorn, Director of Operations. “By incorporating best practices and higher customer service standards, we have been able to support more in-depth interactions with our members, whether that means providing more detailed responses to questions or better educating organizations about the benefits of reimbursing for unemployment claims versus paying taxes.”

“On the heels of this increase in customer service standards was the increase in direct savings that our members experienced last year as well,” said Groh in reference to mitigated unemployment claims costs and cash back to participants.

Last year, UST was able to help members mitigate $32,598,054 in unemployment claims through best-in-class claims management. The same claims management services allowed UST to return an additional $1.7 million of charges made in error by state unemployment offices, which were audited by UST and credited back to the individual organizations.

Select participants also received $11,041,738 in cash back after their reserve accounts were reviewed for positive claims experience.

Her drive and passion to spread awareness within the community makes her a great fit for the UST team. Laurie explains, “I am not doing any volunteer work currently, but when my father passed away from cancer 10 years ago, one of the ways I got through it was to get involved with the American Cancer Society’s Relay for Life fundraisers in Ventura.”

Outside of the office, Laurie and her husband are adjusting to life as newfound puppy parents. They’re rescue puppy, Watson, is a Dachshund/Corgi mix and makes a wonderful addition to their household.

When given the opportunity, Laurie can’t resist the tranquility of nature. “Camping is probably my favorite thing to do and my husband and I go at least twice a year – sometimes more,” she says. “My favorite camping trip was years ago with my sister and some friends and we went on a 50 mile (2 ½ day) river rafting trip on the Colorado River from Grand Junction, CO to Moab, UT…definitely one of the best trips I’ve ever been on!”

In addition to being a dog lover and camping enthusiast, Laurie likes to let loose with a little help from her buddy, Bruce. If her life was a TV show, Laurie would select Growin’ Up by Bruce Springsteen as a theme song that played every time she walked into a room. “This represents the music I grew up with and sometimes I don’t think I’m finished growing up.”

Are you a fan of Bruce Springsteen too? Tell Laurie about it @USTTrust with the hashtag #MeetUSTMondays!

Since the Great Recession took its initial toll on the state unemployment insurance (UI) funds, states across the U.S. have gone into considerable debt in order to provide benefits for millions of unemployed. Trying to combat unemployment costs while restoring their debt with the federal government, many states look towards alternative measures to repair their financial foundations.

In 2011, states accumulated a debt of over $47 billion owed to the federal government– the peak of the United States’ economic deficit. While the federal debt has since decreased, with 16 states still owing over $21 billion at the beginning of 2014, a lot of states took out private loans to avoid an automatic increase in their federal unemployment tax on employers.

With a low UI trust fund balance, many states have been forced to cut their unemployment benefits, rather than borrowing additional money from the government. Other alternative methods used to reach state solvency include:

Such actions were meant to diminish volatility and recover sensibly from the impact of the debt.

While the states have steadily reduced the debts triggered by the Great Recession, the U.S. has a long way to go before they achieve full economic restoration. And employers will continue to see their overall cost of unemployment steadily rising, if their state is to both recover and prepare for the next downturn.

To see how your state unemployment insurance trust fund debt compares to other states, view Stateline’s chart here.

Learn more about how the U.S. is affected by the unemployment trust fund debt here.

What does that mean? Well, by federal law, 501(c)(3)s are allowed to opt-out of paying taxes into their state unemployment tax fund, and instead only reimburse the state if and when they have an actual unemployment claim, dollar-for-dollar.

It can be a savings opportunity for many nonprofits who have lower claims than what they pay in state unemployment taxes—which are often driven up by for-profits and other companies that go out of business, as well as state fund deficits and improper payments made in error.

The Unemployment Services Trust (UST) performed more than 200 free unemployment tax savings evaluations for nonprofits with 10 or more employees in 2013, finding a total of $3,532,485.26 potential unemployment tax savings if they were to exercise their exemption and join the UST program instead.

This year, UST is aiming to identify more than $7 million in unemployment tax savings for nonprofits through free savings evaluations. But time is running out. Most states have a December 1 opt-out deadline, so UST needs all savings evaluation forms submitted before November 15th at the latest in order to meet the state deadline.

You can view your state’s unemployment tax exemption deadline here: www.chooseust.org/state-unemployment-tax-opt-out-deadlines-for-nonprofits

Unfortunately, if a nonprofit misses the state deadline, they have to wait until the following year to exercise their exemption and join the Unemployment Services Trust. So if you or a nonprofit you know has not exercised their exemption, be sure to share the free savings evaluation before the November 15th deadline: www.chooseust.org/request-a-savings-quote